Good employment news plus Social Security solutions

Peek of the Week

Weekly Market Commentary

June 8, 2026

The Markets

There was some good news and some bad news last week.

Let’s start with the good news: Employment gains exceeded expectations last month.

Employers in the United States added 172,000 new jobs in May, similar to April’s 179,000 new jobs. The unemployment rate remained steady at 4.3 percent, the average work-week length was about 34 hours, and wages rose.

“The strong payroll growth, steady unemployment rate, and broad-based job gains are unambiguously good news, but Friday's data did show the labor market still has some weak spots…Those who are out of work are also still finding it difficult to get a job. The share of unemployed workers who have been out of work for 27 weeks or more rose to 27.5 [percent] in May, up from 25.3 [percent] in April and 20.4 [percent] a year ago,” reported Megan Leonhardt of Barron’s.

Here’s the bad news: The Federal Reserve probably won’t lower the federal (fed) funds rate this year. It might raise the rate. (The fed funds rate is the interest rate at which banks lend money to each other. Other interest rates often move in the direction the fed funds rate moves, increasing or lowering borrowing costs.)

The Fed’s two main jobs are to keep employment high and inflation low. Employment is healthy. The long-term average unemployment rate in the U.S. is about 5.7 percent, and the current rate is at 4.3 percent. Inflation, on the other hand, is rising faster than the Fed would like and, in recent months, has accelerated. As a result, the Fed is less concerned about supporting employment and more focused on reducing inflation.

One way for the Fed to fight inflation is to raise the federal funds rate. The move typically pushes other interest rates higher, increasing the cost of borrowing. Higher borrowing costs can slow consumer spending. In addition, higher borrowing costs can reduce company profits. When financial analysts anticipate lower corporate profits, they reassess stock valuations, and stock prices sometimes move lower.

While strong employment numbers are good news for people looking for work, they signal to the Fed that the economy doesn't need the support lower rates might provide. Instead, inflation become the Fed’s primary focus. Historically, higher rates are a tool the Fed has used to bring prices down.

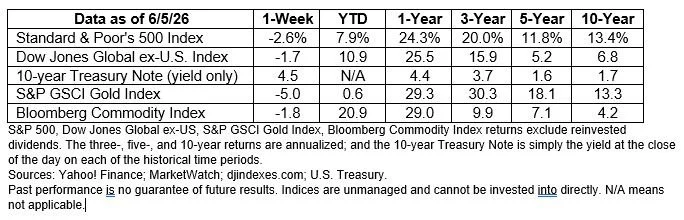

The possibility of higher rates hit financial markets hard last week.

“Wall Street’s historic weekly run came to a halt, with stocks hit by a tech selloff and higher bond yields after a solid jobs report added to bets the Federal Reserve’s next interest-rate move will be a hike. That repricing of the Fed outlook coincided with a swoon in the artificial-intelligence shares that had led a surge from this year’s lows,” reported Rita Nazareth of Bloomberg.

By the end of the day on Friday, major U.S. stock indexes were lower, and yields on all but the shortest maturities of U.S. Treasuries were higher.

SEARCHING FOR A SOCIAL SECURITY SOLUTION. In 2025, the trustees of the Social Security trust fund reported that the fund, “will be able to pay 100 percent of total scheduled benefits until 2033…At that time, the fund’s reserves will become depleted and continuing program income will be sufficient to pay 77 percent of total scheduled benefits.”

As a result, policymakers, researchers, and advocacy groups have been discussing ways to strengthen the program's long-term finances. While there is broad agreement that Social Security's finances should be addressed, there is much less agreement about the best way to address it. As a result, a variety of proposals have emerged, each designed to approach the challenge from a different angle. For example, lawmakers could:

Increase program funding. Increasing the amount of money flowing into the program could help preserve scheduled benefits and improve Social Security's long-term finances. The Peter G. Peterson Foundation highlighted two ways this could be accomplished, including:

· Increasing the payroll tax rate.

· Raising or eliminating the cap on earnings subject to Social Security taxes to include income above $176,100.

Slow the growth of program costs. Another approach is to slow the growth of future program costs. Rather than bringing more money into the system, these proposals seek to reduce future obligations. Among the ideas that have been discussed are:

· Gradually increasing the full retirement age for future retirees.

· Reducing benefits for higher-income retirees or taxing benefits received by higher-income households.

Consider different investment approaches. A third option is to invest the trust funds differently. One recently discussed proposal would create a fund that invests a portion of Social Security's assets in a diversified portfolio of stocks. The idea is that a diversified investment portfolio could generate higher long-term returns than government bonds alone, potentially strengthening the program's finances over time.

At this point, most experts are not focusing on a single solution. Instead, they are evaluating which combinations of solutions might work because a series of modest changes may be easier to implement than one large change. While there is no consensus yet, a solution that combines various ideas could strengthen Social Security's long-term financial health.

WEEKLY FOCUS – THINK ABOUT IT

“A nation’s greatness lies in its possibility of achievement in the present, and nothing helps it more than the consciousness of achievement in the past.”

― Theodore Roosevelt, Former U.S. President

Best regards,

Leif M. Hagen, CLU. ChFC

LPL Financial Advisor

Achievement Financial

Dream. Plan. Achieve.

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this email with their email address and we will ask for their permission to be added.

Securities offered through LPL Financial, Member FINRA/SIPC.

* These views are those of Carson Coaching, not the presenting Representative, the Representative’s Broker/Dealer, or Registered Investment Advisor, and should not be construed as investment advice.

* This newsletter was prepared by Carson Coaching. Carson Coaching is not affiliated with the named firm or broker/dealer.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* All indexes referenced are unmanaged. The volatility of indexes could be materially different from that of a client’s portfolio. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. You cannot invest directly in an index.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the 3:00 p.m. (London time) gold price as reported by the London Bullion Market Association and is expressed in U.S. Dollars per fine troy ounce. The source for gold data is Federal Reserve Bank of St. Louis (FRED), https://fred.stlouisfed.org/series/GOLDPMGBD228NLBM.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* The Dow Jones Industrial Average (DJIA), commonly known as “The Dow,” is an index representing 30 stock of companies maintained and reviewed by the editors of The Wall Street Journal.

* The NASDAQ Composite is an unmanaged index of securities traded on the NASDAQ system.

* International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage is often obtainable in commodity trading and can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee it is accurate or complete.

* There is no guarantee a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

* Asset allocation does not ensure a profit or protect against a loss.

* Consult your financial professional before making any investment decision.

* To unsubscribe from the “Peek of the Week” please reply to this email with “Unsubscribe” in the subject line or write us at Leif@AchievementFinancial.com

Sources:

https://www.bls.gov/news.release/empsit.nr0.htm

https://www.barrons.com/livecoverage/jobs-report-data-may-today?mod=hp_LEDE_C_3 or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/06-08-26-Barrons-Some-Sign-of-Job-Market%20-%202.pdf

https://ycharts.com/indicators/us_unemployment_rate

https://www.bea.gov/data/personal-consumption-expenditures-price-index

https://www.investopedia.com/terms/f/federalfundsrate.asp

https://www.bloomberg.com/news/articles/2026-06-04/asian-stocks-poised-to-edge-lower-oil-steadies-markets-wrap or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/06-08-26-Bloomberg-Nasdaq-100-Sinks%20-%206.pdf

https://www.barrons.com/market-data?mod=BOL_TOPNAV or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/06-08-26-Barrons-DJIA-S&P-Nasdaq%20-%207.pdf

https://www.ssa.gov/oact/TRSUM/index.html

https://www.brookings.edu/articles/fixing-social-security-blueprint-for-a-bipartisan-solution

https://www.pgpf.org/article/lawmakers-are-running-out-of-time-to-fix-social-security

https://crr.bc.edu/can-equity-investments-help-social-securitys-long-run-financing

https://www.trlibrary.com/tr/fake-quotes

Photo by Campaign Creators on Unsplash