Stocks rally after cease-fire as consumers have concerns

Peek of the Week

Weekly Market Commentary

April 13, 2026

The Markets

Sunny with a chance of rain.

Last week, news of a two-week pause in the Middle East conflict was like a sunny day. Investors celebrated and the relief rally lifted U.S. stocks higher. “The cease-fire announced on Tuesday led to the best day for the stock market in almost exactly a year,” reported Avi Salzman of Barron’s.

On Friday, though, some clouds appeared on the horizon. U.S. economic data and Middle East damage assessments gave investors pause, and the market’s advance slowed as they considered the potential impact of:

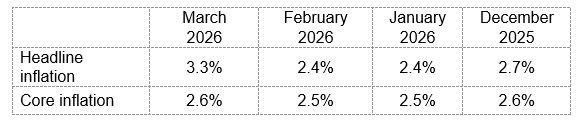

Rising inflation. The Consumer Price Index showed that prices surged from February to March. Gasoline and fuel oil prices were up 18.9 percent and 44.2 percent, respectively.

The good news was that core inflation, which excludes volatile food and energy prices, remained relatively steady. “There was no doubt that the spike in gasoline prices was going to drive up price growth in March, but the latest data show the Iran war's effects on inflation were largely contained to energy, at least for now,” reported Megan Leonhardt of Barron’s.

An all-time low for consumer sentiment. Consumer optimism bottomed out in early April, falling 11 percent from month to month and 9 percent from year to year. Surveys of Consumers Director Joanne Hsu wrote:

“Demographic groups across age, income, and political party all posted setbacks in sentiment, as did every component of the index, reflecting the widespread nature of this month’s fall. One-year expected business conditions plunged about 20 [percent] and is now 6 [percent] below last April. Assessments of personal finances declined about 11 [percent], with consumers expressing a substantial increase in concerns over high prices and weaker asset values.”

There is a caveat. Most of the interviews for the survey’s initial monthly reading were conducted before the ceasefire announcement. If the ceasefire holds, sentiment could improve over the month.

Energy infrastructure damage assessments. With a two-week ceasefire underway, “…people are waking up to the fact that the war will cause lasting damage...Most obviously, Iran’s control of the Strait of Hormuz is now a fact, and something of which it is taking full advantage. Secondly, a lot of energy infrastructure in the region has been damaged since the war erupted, and some of it will take time to repair,” reported Robin Wigglesworth of the Financial Times.

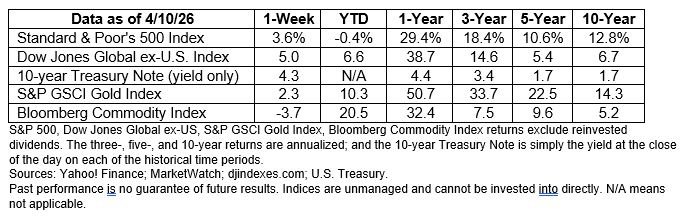

Despite Friday’s retreat, major U.S. stock indices finished the week higher. In addition, yields on most maturities of U.S. Treasuries moved lower over the week.

THERE’S A NEW TYPE OF RETIREMENT ACCOUNT AND IT’S FOR KIDS. The One Big Beautiful Bill Act, which passed into law last summer, created a new type of retirement account known as the “Trump account”. Here’s what you need to know:

Who is eligible?

These accounts can be opened for any child who is younger than 18-years-old and has a Social Security number. To qualify the child must be age 17 or younger for the entire calendar year in which the account is opened, reported the Schwab Center for Financial Research (SCFR).

Who can contribute?

The U.S. Treasury will contribute $1,000 to the accounts of children born in the U.S. between January 1, 2025, and December 31, 2028, reported the Center for Retirement Research at Boston College (CRRBC).

Additional contributions (up to $5,000 each year) can be made by:

· Parents,

· Grandparents,

· Account beneficiaries,

· A parent or child’s employer (up to $2,500 that counts toward the annual limit),

· Charitable organizations (not subject to the $5,000 limit), and

· Federal, state, and local governments (not subject to the $5,000 limit).

Are contributions taxable?

It depends on who makes the contribution. Parents, grandparents, and other individuals do not get a tax break for contributions. However, contributions made by employers or other entities are made on a pre-tax basis, according to the CRRBC.

When can the money be withdrawn?

These accounts are intended to help young Americans fund their retirements. As a result, investment choices are limited and contributions cannot be withdrawn before the beneficiary reaches age 18. At that point, the account is subject to the same contribution rules as traditional IRAs, which means the account holder will owe taxes on any distributions, reported SCFR.

How much could an account be worth at retirement?

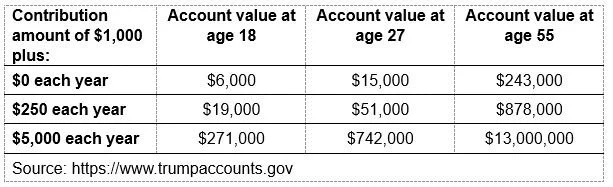

It’s difficult to know. The account value will depend on how much is contributed and how investments perform over time. The U.S. government’s website estimates account values at various ages, assuming an average annual return of for the Standard & Poor’s 500 Index. The average return is about 10.6 [percent], which reflects the returns from 1957 through 2025, reported J.B. Maverick of Investopedia. Here’s what they estimate:

Is it better to contribute to a Trump account, a Roth IRA, or a 529 plan? It all depends. While the free money available to newborns is attractive, other types of accounts may offer greater flexibility and better tax advantages, reported Abby Schultz of Barron’s.

If you would like to learn more about ways to help young Americans save and invest for the future, please get in touch.

WEEKLY FOCUS – THINK ABOUT IT

“The best time to plant a tree was 20 years ago. The second best is now.”

– Oxford Treasury of Sayings and Quotations

Best regards,

Leif M. Hagen, CLU, ChFC

LPL Financial Advisor

Achievement Financial

Dream. Plan. Achieve.

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this email with their email address and we will ask for their permission to be added.

Securities offered through LPL Financial, Member FINRA/SIPC.

* These views are those of Carson Coaching, not the presenting Representative, the Representative’s Broker/Dealer, or Registered Investment Advisor, and should not be construed as investment advice.

* This newsletter was prepared by Carson Coaching. Carson Coaching is not affiliated with the named firm or broker/dealer.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* All indexes referenced are unmanaged. The volatility of indexes could be materially different from that of a client’s portfolio. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. You cannot invest directly in an index.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the 3:00 p.m. (London time) gold price as reported by the London Bullion Market Association and is expressed in U.S. Dollars per fine troy ounce. The source for gold data is Federal Reserve Bank of St. Louis (FRED), https://fred.stlouisfed.org/series/GOLDPMGBD228NLBM.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* The Dow Jones Industrial Average (DJIA), commonly known as “The Dow,” is an index representing 30 stock of companies maintained and reviewed by the editors of The Wall Street Journal.

* The NASDAQ Composite is an unmanaged index of securities traded on the NASDAQ system.

* International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* The risk of loss in trading commodities and futures can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. The high degree of leverage is often obtainable in commodity trading and can work against you as well as for you. The use of leverage can lead to large losses as well as gains.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee it is accurate or complete.

* There is no guarantee a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

* Asset allocation does not ensure a profit or protect against a loss.

* Consult your financial professional before making any investment decision.

* To unsubscribe from the “Peek of the Week” please reply to this email with “Unsubscribe” in the subject line or write us at Leif@AchievementFinancial.com

Sources:

https://www.barrons.com/articles/war-inflation-stock-market-df2a811a?mod=hp_LEDE_B_1 or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/04-13-26-Barrons-War-Inflation-%201.pdf

https://www.bls.gov/news.release/cpi.nr0.htm

https://www.bls.gov/opub/ted/2026/consumer-prices-up-2-4-percent-over-year-ended-february-2026.htm

https://www.bls.gov/news.release/archives/cpi_01132026.htm#

https://www.barrons.com/livecoverage/inflation-report-cpi-data-march-fed-rate-cuts/card/inflation-wasn-t-as-bad-as-feared-why-it-won-t-make-the-fed-s-life-easier--KY53ecxD2vNCA3qsUkA9 or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/04-13-26-Barrons-Inflation-Wasnt-as-Bad%20-%206.pdf

https://www.sca.isr.umich.edu or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/04-13-26-UoM-Survey-of-Consumers%20-%207.pdf

https://www.ft.com/content/73deaed8-4458-426f-955c-00f5be73ce69 or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/04-13-25-Financial-Times-Surveying-The-Middle-Easts%20-%208.pdf

https://www.barrons.com/market-data?mod=BOL_TOPNAV or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/04-13-26-Barrons-DJIA-S&P-Nasdaq%20-%209.pdf

https://www.schwab.com/learn/story/ins-and-outs-new-trump-kids-accounts

https://crr.bc.edu/trump-accounts-a-primer-for-parents/

https://www.investopedia.com/ask/answers/042415/what-average-annual-return-sp-500.asp

https://www.barrons.com/articles/trump-accounts-advantages-disadvantages-603f9f82? or go to https://resources.carsongroup.com/hubfs/WMC-Source/2026/04-13-26-Barrons-Trump-Accounts-May-Come%20-%2015.pdf

Ratcliffe, Susan, Oxford Treasury of Sayings and Quotations, October 13, 2011 or go tohttps://resources.carsongroup.com/hubfs/WMC-Source/2026/04-13-26-Oxford-Treasury-of-Sayings%20-%2016.pdf